Can the ‘Wild West’ of ethical investment be tamed?

Khartoum’s Presidential Palace was just a short stroll away from the outdoor restaurant where Jeff Quartermaine started scrolling his phone for the latest news headlines.

Having spent what seemed to be a normal morning on the streets of the Sudanese capital, the managing director of ASX gold miner Perseus was stunned by what he read on major international news websites while he enjoyed his lunch.

Perseus boss Jeff Quartermaine says “quite often, stories are generated by people who have a particular agenda to push ...“. Philip Gostelow

“It said the Forces for Freedom and Change (FFC) had implemented a program of civil disobedience,” he recalled, in reference to the pro-democracy group that has spent the past six months protesting the African nation’s latest military coup.

“[According to the reports,] there were roadblocks throughout Khartoum, 50 per cent of shops and buildings were closed and there was no traffic on the streets. I am sitting right in the middle of this and it’s not happening at all.”

The influence of headlines

Quartermaine doesn’t pretend that Sudanese politics is free of tension; barely a decade after a brutal civil war, inter-tribal conflicts persist while two military coups in the past three years have ensured that pro-democracy protests around the Presidential Palace are common.

Photographs published by the likes of BBC and the New York Times make clear that violent clashes have occurred between pro-democracy campaigners and the ruling junta.

“This was one anecdote I had on one day of the year and things might be different at other times,” he says.

“But it just gives you an indication that what comes out isn’t necessarily the case and quite often, stories are generated by people who have a particular agenda to push and it isn’t necessarily consistent with what is actually occurring.”

Dispatches filed from Sudan by the likes of Al Jazeera, the BBC and Chinese agency Xinhua will in future affect more than Quartermaine’s lunch.

Perseus is in the process of buying its first Sudanese gold deposit, and negative headlines out of Sudan will feed directly into the environmental, social and governance (ESG) ratings that increasingly influence investors’ opinions and the cost of capital.

The rising influence of ESG ratings reflects the fact that most investors want to put their money into things that are both ethical and profitable.

But a lack of regulation, standardisation and transparency in the fast-growing sector has left many concerned that investors will be led astray while conflicts of interest go unchecked.

The billion dollar industry

BHP chief executive Mike Henry ignited the debate locally earlier this month when he said there was a lack of aligned standards and engagement across the surging number of ESG ratings agencies in the market.

Henry’s concerns, which Quartermaine shares, are similar to the findings published in November by the International Organisation of Securities Commission (IOSCO), which is the global league for regulators like the Australian Securities and Investment Commission.

IOSCO believes the ESG ratings industry became a billion dollar industry for the first time in 2021, and the ratings produced are a pivotal part of the much bigger industry that creates ESG funds and indexes.

The concerns are even shared by some within the ESG rating sector like Simon MacMahon, who is head of ESG research for Morningstar’s “Sustainalytics” business.

“There is quite a number of us and different ratings agencies have different approaches, they are using technology in different ways, they have different capabilities, different bench strength and sizes but everybody gets painted with the same brush sometimes which is unfortunate,” he says from Toronto.

“We fully expect and we understand that we are going to be regulated at some point in the not [too] distant future and it is not something we disagree with actually, the important thing for us is that the regulations are smart and targeted.”

To understand why governments in Europe and North America are moving toward regulation of ESG ratings agencies, you first have to understand what they do.

‘More harm than good’

Firms like Sustainalytics generate most of their revenue by selling subscriptions to institutional investors in exchange for a frank assessment of the non-financial risks that companies are exposed to, and the extent to which companies have systems to manage those risks.

The work is analogous to that which traditional credit rating agencies like Fitch and Moody’s do on the financial risks facing a company and, not surprisingly, most of the traditional credit ratings agencies have become major producers of ESG ratings too.

But some credit rating agencies like Kroll have fiercely criticised their peers’ moves into providing ESG ratings, saying “ESG ratings in their current form are doing more harm to the market than good”.

Kroll incorporates ESG factors into its credit ratings, but does not publish ESG ratings as a discrete product. It fears that scoring things that are inherently qualitative will be hopelessly subjective across different ratings agencies.

“It is hard to imagine a single ESG score that encapsulates an issuer’s E, S, and G profile, because those things mean different things to different people,” said Kroll’s chief ESG adviser, Pat Welch, in an article published earlier this month.

As a case in point, Kroll said the range of ESG scores given to a company tend to be statistically wider than the range of different credit scores they receive.

Not a one size fits all

Sustainalytics employs close to 500 analysts to collect information on about 4500 companies worldwide.

ESG might be an anagram of three words, but MacMahon says there are around 20 “material factors” that companies are judged upon, from their impact on biodiversity to workplace safety, their relationships with unions and their carbon footprint.

The analysts score the information they collect under a prescribed methodology to reach a numerical ESG risk score for the company they are rating.

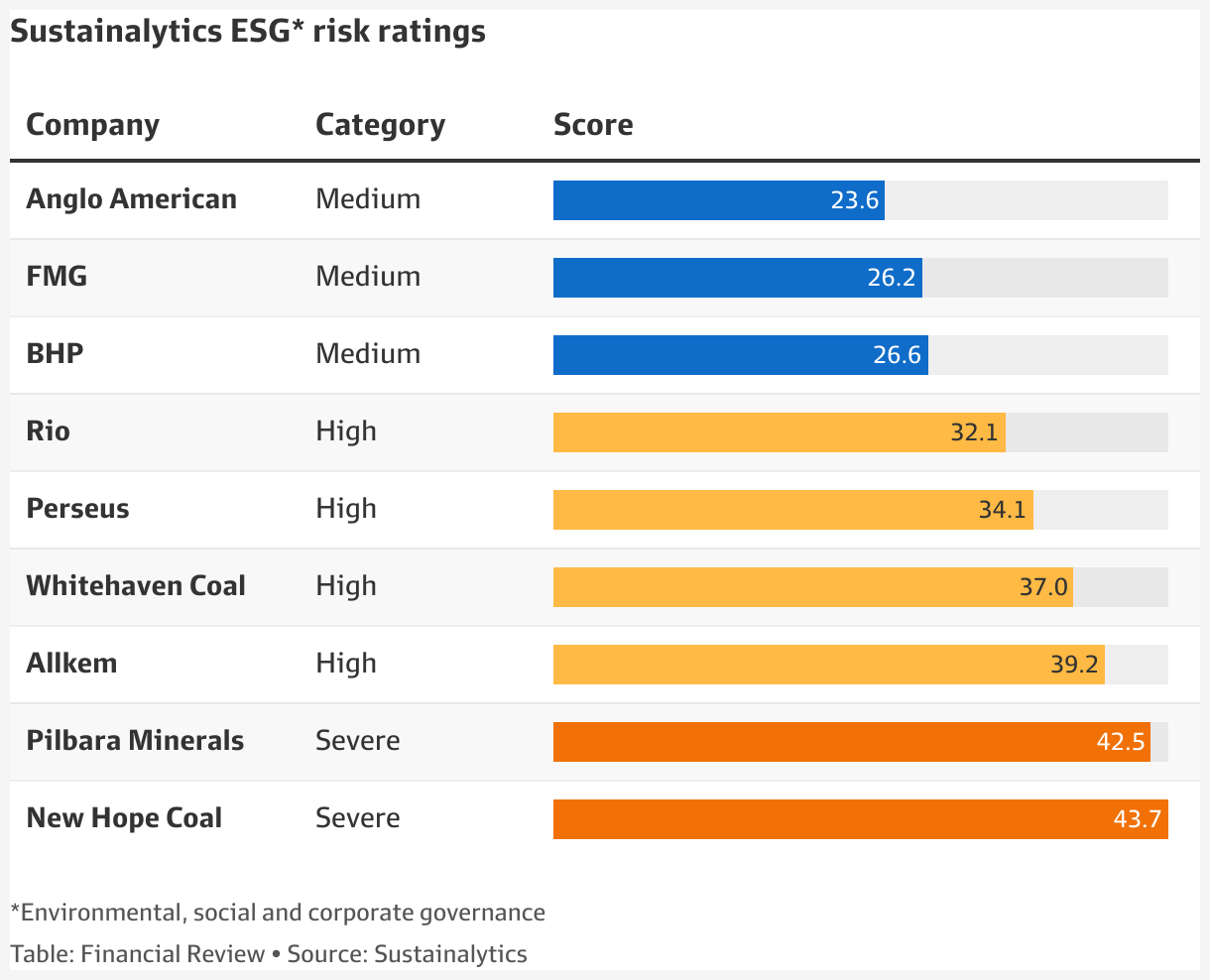

The score places the company on Sustainalytics ESG risk spectrum, which is broken into five categories; negligible, low, medium, high or severe.

The commercial relationship between ratings agencies like Sustainalytics and investors like Janus Henderson resources fund manager Tal Lomnitzer is effectively the same as that between a newspaper and its subscribers.

“We do subscribe to a number of third-party providers. They all have slightly different ratings and approaches and there is a bit of an alphabet soup out there,” says Lomnitzer.

“It is useful to keep an eye on the averages of them and they often, as a first port of call, present a really easy way of looking at a company and calling out some specific things we might want to dive deeper into alongside our own analysis”.

But IOSCO warned that conflicts of interest could emerge where ESG ratings agencies also sell other services to the companies that are subject to their ratings.

Sustainalytics’ revenue stream

Some ESG rating agencies offer advisory services that promise to help companies improve the ratings they publish; an offer that some executives interpret as a subtle form of blackmail.

“This could result in conflicts of interest where the consulting side of business may provide information to the company to allow said company to gain an advantage in terms of receiving a good rating,” said IOSCO in its November final report.

While Sustainalytics primary revenue stream is from subscriptions to institutional investors, MacMahon says Sustainalytics does have a small revenue stream from the companies it rates.

“If companies want to use their rating for either marketing or capital raising purposes they pay us a licence [fee] in order to be able to do that,” he says.

Sustainalytics also earns revenue by providing second opinions on the ESG credentials of green bonds; fundraising initiatives that are tied to a particular investment that will create environmental benefit.

IOSCO said its members should consider expanding their regulatory regimes to incorporate ESG ratings agencies.

The United Kingdom government has signalled that in future ESG ratings firms will be regulated by the Financial Conduct Authority (FCA).

The FCA’s equivalent in Europe, ESMA, has asked the European Commission for more power over ESG ratings agencies because there was “a need to match the growth in demand for these products with appropriate regulatory requirements to ensure their quality and reliability”.

ASIC to watch developments

The United States Securities Exchange Commission (SEC) created an “ESG task force” last year designed to find ESG related misconduct and ESG ratings were one of the key focuses of the annual review of credit rating agencies that the SEC published in January.

MacMahon says Sustainalytics welcomes the trend toward more regulation.

“We think they [regulators] should probably focus primarily on things like a standard minimum in terms of the level of quality,” he says.

“Some transparency of methodologies so the people using the ratings have an understanding of what they are seeing and just a basic management of conflicts of interest.”

ASIC is a member of IOSCO and said it would watch developments abroad with interest, but currently Australia has no apparent plan.

“Like any other agency, licensed or not, they are obviously not allowed to issue false or misleading information, manipulate the market, or engage in other acts of dishonesty. Where warranted, ASIC takes action against any such breaches,” said an ASIC spokesman.

“But leaving aside that general requirement to act lawfully, there is no specific regulation applying to ESG ratings providers. Any move to change that would be a matter for government and the parliament.”

While ESG rankings matter for all companies they are particularly challenging for mining and energy companies, whose work often takes them into frontier locations and usually requires the disturbance of landscapes to extract the saleable product.

“ESG is particularly important in an extractive industry where one relies on the willingness of host countries to let you come in and develop their resource; the non-financial aspects of operating can be an existential threat if you drop the ball,” says Lomnitzer.

The rise of ESG

When BHP chairman Ken Mackenzie tries to quantify the rising influence of ESG, he paints a picture of how the seating arrangements have changed over the past decade at the regular meetings between companies and institutional investors.

A decade ago, Mackenzie’s fictional ESG analyst would sit at the back of the room, quietly listening and taking notes on the conversation between the chief investment officer and the chief executive.

Within five years, the ESG analyst had earned a seat at the table and the right to ask a couple of questions.

Nowadays, Mackenzie reckons, the ESG analyst holds court as the star of the show.

PWC’s head of mining, Debbie Smith, told the Financial Review Business Summit last week that the momentum was unstoppable.

“The new breed of investors stands poised to punish weak ESG and reward the strong so my advice is throw away your risk umbrella and lean into ESG,” she said.

“Here in Australia, we are standing on the brink of an ESG transformation that is every bit as far-reaching as the digital transformation. Join the ESG innovators because if you don’t, the divide between leaders and laggers will only grow until catching up is virtually impossible.”

Flaws in ESG rating

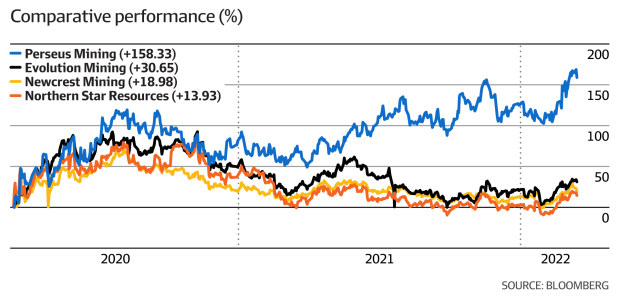

Asked whether ESG ratings were having an impact on Perseus, Quartermaine recounts an example where a top 20 shareholder was almost forced to divest its stake twice in the past 13 months because the investor’s mandate required it to screen out companies with a certain ESG rating.

Perseus was perilously close to slipping below that mandated threshold in the mind of one ESG rating agency, leaving the investor on the brink of selling.

“I had this very lengthy conversation with their fund manager, who expressed great appreciation at the work we had done and said we were doing an excellent job. But he also said if our ESG rating was to fall, he would have to divest the stock, not withstanding the fact we were the top performer in his portfolio,” recalls Quartermaine.

The selldown was averted when Quartermaine tracked down the ESG rating agency and pointed out the flaws in their rating, which he said was based on information that was a year old.

The ESG agency had never visited Perseus’ mines in Ghana and Cote D’Ivoire nor the health clinics and classrooms the company has built for the communities near its mines.

The agency had not told Perseus of its intention to publish a rating, nor that the rating had been published until it was approached by Perseus.

He would have missed out on a very, very large capital gain.

— Jeff Quartermaine, Perseus

“It would have mattered for us, but it would have mattered even more for the investor because they would have lost an opportunity,” says Quartermaine in reference to the 61 per cent surge in Perseus shares over the past year.

Frustration among miners

Shares in gold mining rivals like Northern Star, Newcrest and Evolution rose by between 12 per cent and 15 per cent over the same period.

“He would have missed out on a very, very large capital gain.”

The verdicts reached by ESG ratings agencies are a common source of frustration and confusion among those who run Australian mining companies.

Sustainalytics puts Australian lithium miners like Pilbara Minerals and Liontown into the “severe” ESG risk category, despite the fact their investment proposition is built around helping the world to decarbonise by supplying the critical minerals needed for electric vehicles and energy storage.

Sustainalytics gave exporters of Australian thermal coal like Whitehaven and Glencore a more favourable ranking than the lithium miners, placing the coal miners in the “high” risk category.

MacMahon says Sustainalytics’ traditional institutional audience understands the wide range of factors that make it possible for a theoretical coal miner to get a better ESG rating than a lithium miner.

“They [subscribers] have a level of sophistication and investment where this is not confusing for them at all,” he says.

But the ratings may be less well understood by others.

“I do think ESG is becoming a tool for many other types of investors, many other types of financial actors who are coming up the curve in terms of understanding the nuances of ESG, the various different ways it can be used,” says MacMahon.

“It is important that whoever is using ESG information and ratings really understands what they are looking at.”

Information that is out of date

MacMahon says ESG ratings rely heavily on company disclosures, so companies concerned about their ranking can help themselves by being more transparent.

“ESG is fundamentally quite handicapped in its ability to create assessments because the ESG disclosures coming from companies are very incomplete and in some cases not of high quality,” he says.

“We have seen a dramatic increase in the amount of disclosures coming from companies over the last decade, so that is great, but I don’t think right now the increases we are seeing are fast enough.”

The heavy reliance on information reported by companies has meant that ESG ratings are typically updated infrequently and with information that is often out of date.

“Shareholders are left assessing the ESG performance of companies on their annual report by and large, so quite often there is a year gap between updates,” says OZ Minerals chief Andrew Cole.

Last year’s creation of the International Sustainability Standards Board (ISSB) could make a big difference by forcing companies to report ESG information in a standardised way, much as the International Accounting Standards Board has sought to do for financial reporting.

That would make life much easier for ESG ratings agencies – and investors – when trying to compare and contrast the ESG credentials of multiple companies.

MacMahon says companies concerned about their ESG rating can also help themselves by engaging with ESG firms when approached for clarification or feedback.

“Going back to 2008 or 2009, it used to be that only about 10 per cent of companies responded to our request for feedback and I think the number now is well over 50 per cent, which I think is just a testament to how much more relevance ESG ratings have than they did back then,” he says.

But Kroll argues that many small- and medium-sized companies don’t have the staff nor the time to respond to the information wishlists of ESG ratings firms, and that means ESG ratings will be unconsciously biased towards the biggest companies that have the resources to explain and defend themselves.

“Large entities often have significantly more time and resources to complete the multitude of ESG surveys and disclosure requests they receive. Small and mid-sized issuers, on the other hand, do not have the same ability, and they are often penalised for not having the same means to fill out the requested information,” said Kroll earlier this month.

Company disclosures can be unreliable, biased, or mask risks. This is where RepRisk can shine a light on these hidden risks.

— Swiss firm RepRisk

A more rebellious segment of the ESG rating industry don’t want to be captive to the information that companies publish about themselves in annual reports.

Some like Swiss firm RepRisk deliberately exclude the information that companies disclose in the belief that they can get a better picture of ESG risks by scanning more than 100,000 media and regulatory publications every day across 23 languages.

“By relying primarily on company self-reported data, private market firms might not be getting the full picture. Company disclosures can be unreliable, biased, or mask risks. This is where RepRisk can shine a light on these hidden risks,” the Swiss firm says in promotional material on its website.

While artificial intelligence does the heavy lifting at RepRisk, the firm also employs more than 100 analysts to apply a human lens on the controversies identified by mass scanning of the internet and the world’s media.

The human touch is important in cases like Rio Tinto’s recent report into workplace culture, where a survey of staff found the company had been plagued by bullying, racism and sexual harassment over the past five years.

Addressing the issue

The report confused many of the less sophisticated ESG algorithms that are heavily reliant on media headlines; coverage of the Rio report contained all the sorts of keywords that algorithms normally identify as negative indicators.

But those negative indicators were coming to light because of a report that Rio commissioned and published in full with an accompanying vow to fix the problem.

Did the Rio report reveal a company with a toxic culture? Or a transparent company proving it was committed to reforming the errors of the past?

“While that was quite shocking to read in some senses, what impressed me about it was that it was independent and published in full, which to me says the company is confronting this issue head on, which is very much a change from what the previous management were doing,” says Lomnitzer.

RepRisk is one of the ESG rating agencies used by Janus Henderson’s resources fund and Lomnitzer reckons it helps his team to monitor risks, even if some of the media reports it collects are less credible than others.

“RepRisk is how we try to track and identify controversies as they are emerging, which can suffer a little bit from that thing about the local newspapers being a rumour mill, however we think the value is in what it brings up for us to then interpret,” he says.

“[RepRisk] is something that has been very useful to us over time because it finds things before other people find things.”

Room for improvement

Glencore boss Gary Nagle says “false reporting” is a common trigger for interaction between his company and the agencies that rate its ESG credentials.

“We embrace the way they review us, we embrace what they want, we are part of that journey,” he says.

“It’s not only about ratings, we want to do the right thing, and when we do the right thing, it drives the ratings.”

Sustainalytics also use artificial intelligence to comb through news articles, but MacMahon says that process is “mostly about accelerating our ability to process information before it gets to our analysts”.

South32 chief executive Graham Kerr believes there is room for improvement in both corporate disclosures and the way companies are rated by the ESG agencies.

“I think there is fault on both sides,” he says.

“There is not a uniform framework at the moment, there is probably [some] maturing that needs to occur.

“Hopefully there can be more of an agreed framework, more of an agreement to talk about this stuff.”

‘Clear set of standards’

Cole said he was inclined to take the blame if external parties were struggling to understand OZ Minerals’ ESG credentials.

“I believe it is my accountability to demonstrate to our shareholders and the market how we are performing and if the market doesn’t understand that then I need to work out what it is I am, or am not saying or demonstrating that helps the market understand that,” he says.

Having ignited the debate, BHP’s Henry also has a solution.

“You fix the problem by leaders in capital markets, leaders in the resources sector, leaders from other [sectors], coming together more effectively to define those standards and then there needs to be the right way of assessing companies against those standards,” he says.

“The ideal is that there is a comprehensive, clear set of standards that define what ‘good’ looks like across multiple ESG dimensions.”

Quartermaine is hopeful that Perseus’ rising profile in the investment community and its constant efforts to improve disclosure will help it win the ESG game.

But as he hopes for the best, he is preparing for the worst, and won’t let his business strategy be hijacked by an ESG score produced by someone who has never visited any of his company’s assets.

“I expect there will be a backlash [from ESG analysts over the investment in Sudan] because a lot of people will derive their knowledge from historical news reports like coverage of [the civil war in] Darfur at the turn of the century,” he says.

“By going into Sudan, Perseus is the first international, professional mining company to come onboard, we will be contributing substantially to their economy, not only through taxation and royalties and the like, but through employment, through purchasing locally and education of people.

“We are willing to do it, but the price for us as a mining company is significant.

“We recognise there are risks around it, but the benefit outweighs the risk and we are more than happy to take on the role of being first mover and demonstrate that having a viable mining industry is a major plus for the development of Sudan as a country.

“If an ESG agency wants to criticise us for doing that, so be it, but we actually believe what we are doing is net positive.”

Subscribe to gift this article

Gift 5 articles to anyone you choose each month when you subscribe.

Subscribe nowAlready a subscriber?

Introducing your Newsfeed

Follow the topics, people and companies that matter to you.

Find out moreRead More

Latest In Energy & climate

Fetching latest articles